Today we’ll take a look at why we think Amcor (ASX AMC) is a good stock to own.

Amcor is an established business with revenue from all over the world.

Even though they are already a market leader, Amcor continues to grow via strategic acquisitions.

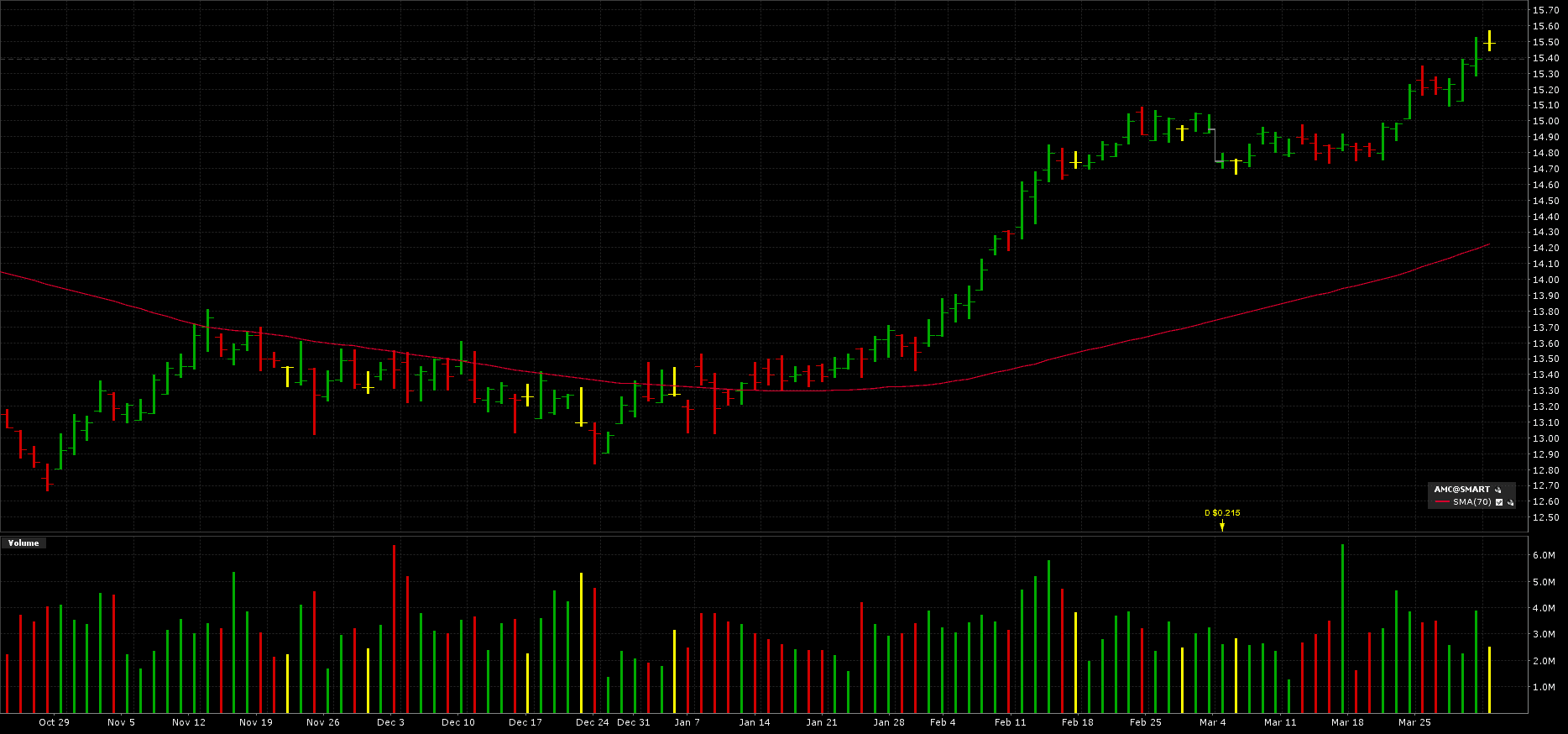

AMC has been on a strong run since October 2018, when it was trading around $13.

AMC is now trading at about $15, a rally of over 15%. Impressive for a company fo its size.

Now let’s get right into it.

Table of Contents

About Amcor (ASX AMC)

Amcor Limited (ASX AMC) is a leading global packaging company with good growth potential. Amcor develops and produces a range of packaging related products and services, involving packaging for food, beverage, pharmaceutical, medical device, and home and personal care, such as rigid containers and specialty cartons.

Amcor has 35,211 employees generating more than USD 9 billion in sales with operations in Australasia, North America, Latin America, Europe, and Asia. Amcor has strong relationships with major customers including large beverage companies like Evian, Nestle, and Coca Cola.

Amcor Core Business

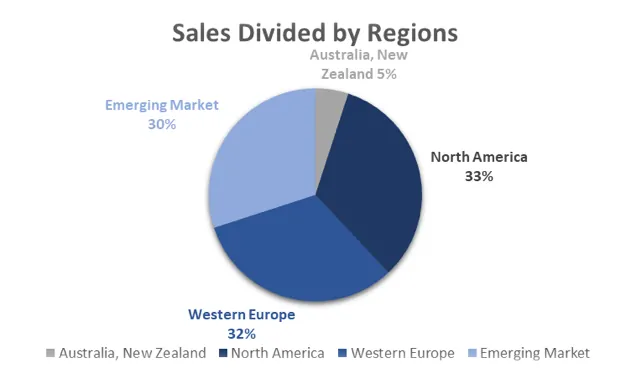

The core businesses of Amcor are flexible packaging, rigid plastic containers, specialty cartons and closure. In FY18, the total sales from these four segments are USD 9.3 billion. As illustrated in Figure 1, flexible packaging and rigid plastic containers make up 55% and 28% of total sales, respectively. Most of the sales are generated overseas, with almost equal contribution from North America (33%), Western Europe (32%) and emerging market (30%).

Figure 1. Sales Divided by Segments

Figure 2. Sales divided by Regions

Industry Trend

Figure 3. Global Containers and Packaging Market Value

Source: all the data are collected from Marketline (Source)

The global packaging market is expected to experience stable growth. As illustrated in Figure 3, from 2013 to 2017, the packaging market has grown by an average of 4.08% year on year. In FY17 rigid plastic made up 40% of the total market value, followed by flexible plastic at 26.3%.

Compared to some of the developed countries which is experiencing market saturation, Asia Pacific is undergoing rapid growth with 40% of the total packaging market. In particular, China and India will play a vital role in the packaging market in the next five years.

The market value of packaging is estimated to be nearly $1800 billion in 2022, up by 23% from 2017.

Strategic Position

Figure 4. Track Record of Growth by Acquisition

Notes: Spend based on announced notes

Source: Amcor 2018 Full Years Results Page 45

Amcor is ramping up its acquisitions. As illustrated in Figure 4, Amcor has done massive acquisitions. Amcor has completed 26 acquisitions during the past six years. In FY16-17 the acquisition target has shifted from Flexible Asia Pacific to Flexible Americas and Rigid Plastics.

On 6 August 2018, there was an announcement that Amcor will merge with Bemis in an all-stock transaction. This acquisition expands its business in the North America Market.

Acquisitions allow Amcor to expand into the US. Amcor will merge with Bemis. Bemis is one of the leading companies in flexible packaging with a 2.03% market share. The transaction will be completed in the first quarter of 2019 and the global sales of Amcor on flexible packaging will increase remarkably.

As illustrated in Table 1, New Amcor’s global sales revenue is projected to reach $ 8.8 billion, with 87% of the growth directly coming from the Bemis’ market in the US. The acquisition of Bemis will help Amcor enter the US market quickly.

Table 1. Regional USD Sales Revenues

Note: Revenue in USD billion and based on CY17 revenue; Amcor revenues exclude specialty cartons; Bemis account based on Amcor estimates of CY17 revenues.

Source: Source: Amcor Limited 2018 AGM slide pack

Acquisitions bring cost synergies. Acquisitions may increase the economics of scales and lower cost. By acquiring Bemis, 50 flexible packaging plants which are worth USD 4 billion will be added to Amcor’s portfolio. Moreover, the cost of procurement will decline as Amcor will have more negotiating power with its suppliers due to its will-be-huge volume on raw material.

Overall, an estimated USD$180M cost synergies could be brought in. The annual saving on cost is expected to reach US$65m in the first year and US$180m (nearly 5% of the sales revenue of Bemis) from the third year. As illustrated, cost synergies come from procurement (40%), G&A Costs (40%) and manufacturing footprint (20%).

Figure 5. Estimated USD 180 Million Cost Synergies

Notes: All data refer to pre-tax cost synergies. Incremental to Bemis “Agility” improvement plan. Any additional synergies would be additive to the transaction metrics.

Recyclable technology and Sustainability. As a leading global company, Amcor has more than 1700 active patents. In the past three years, it has won over 30 awards for innovation.

With investments in research, Amcor pledged that it would achieve fully recyclable and reusable on its packaging by 2025 by increasing the percentage usage of recycled material.

Amcor is the first company with such claim in the world, and this promise could hedge against the regulation risk of increased tax on plastic packaging.

During 2017/2018, MSIC Global Sustainability index has upgraded the level of Amcor to ‘AA’ from ‘A’.

Business Risks

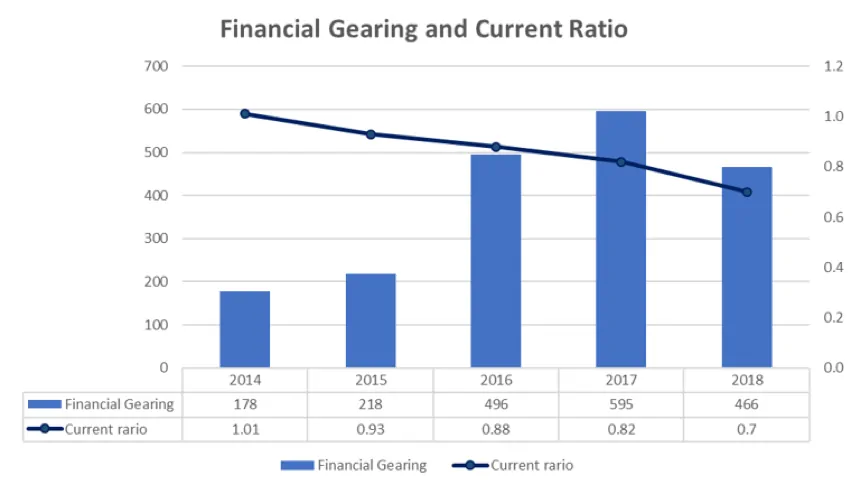

Figure 7. AMC – Financial Gearing and Current Ratio

Amcor supports its aggressive acquisition through borrowing, which weakens its short-term and long-term repayment ability. As illustrated in Figure 7, financial gearing increases from 178% to 466% FY14-18, while current ratio decreases from 1.01 to 0.7.

Amcor’s financial gearing has shown an upward trend in the past five years and reached its peak in 2017. Although it declined slightly in 2018, it still at a high level, which means that Amcor’s long-term debt pressure remains high.

The price fluctuation of raw material may affect the profitability of Amcor. Amcor is exposed to a variety of raw material cost factors, including aluminium, resins and several other raw materials.

Although Amcor passes the raw material pricing fluctuation to downstream customers through up-and-down adjustment contracts, Amcor still faces the problem of not being able to pass the cost in a timely manner. For example, Amcor’s financial loss is largely due to the rise in oil price, which drove up the price of resin, the main materials used in packaging.

Greener production but higher cost. Amcor’s sustainability plan may further weaken the cost control. To achieve 100% recyclable or reusable packaging in 2025, Amcor has to use more expensive materials and follow more complex procedures, which may have negative impacts on Amcor’s margin.

Financial Performance and Peer Comparison

(Notes: all the data below are collected from Morningstar Database and Orbis Database.)

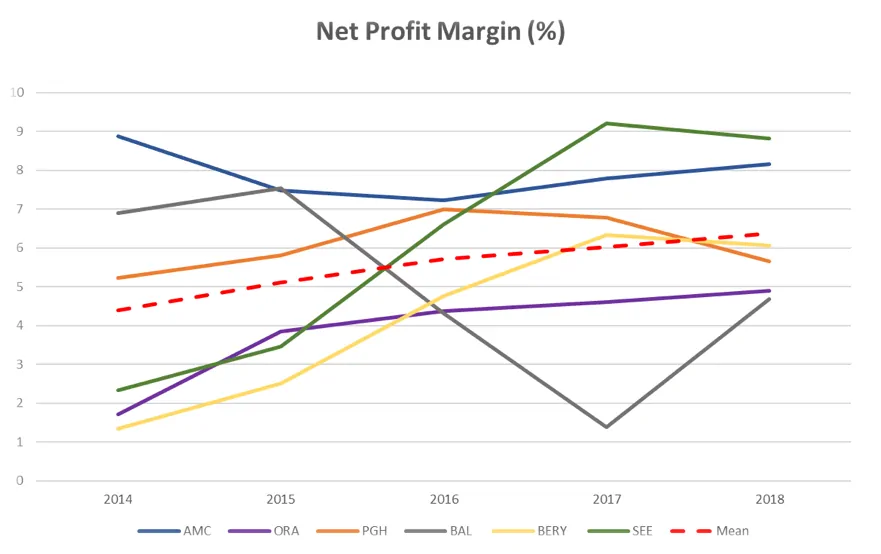

Peer selection. Amcor’s peers are selected from large global packaging suppliers who have similar business strategies to Amcor’s (acquisitions and innovations). Selected competitors include Orora Limited (ASX ORA), Pact Group Holdings LTD (ASX PGH), BALL Corporation (NYSE BAL), Berry Global Group Inc (NYSE BERY) and Sealed Air Corporation (NYSE SEE).

Consistently high net profit margin. The net profit margins of Amcor (blue) decreased from 9 to 7 before recovering to 8 per cent in FY18. Amcor’s net profit margin is consistently higher than most of its competitors FY14-18 and it ranks second in FY18.

High ROE. Amcor’s ROE (blue) is consistently over 40% during FY14-18. Although Berry Global Group (yellow) surpassed Amcor in 2016, Amcor ranked the top in the following two years. As the global packaging industry is expected to grow by 4% in 2019, Amcor’s ROE is likely to stay above 60%.

High but volatile EPS growth. In the last four years, Amcor’s compound EPS growth rate calculated through geometric average method has exceeded 50% p.a.

However, high volatility was seen in EPS growth, as shown in table 2. EPS growth reached as high as 138% and as low as -61%.

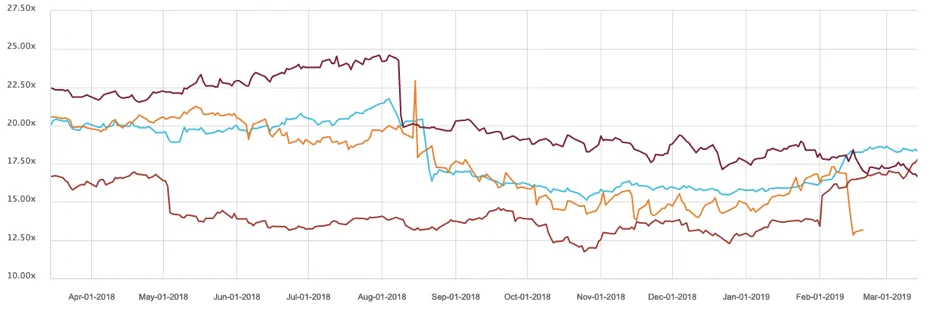

Moderate P/E. In the last year, Amcor’s P/E fell from 20x to 18x and rose slightly to about 19. Its competitors lie similarly within 15-25. Amcor looks to be fairly priced.

Source: S&P IQ Capital

Amcor is a Good Stock at a Justified Price

Amcor is a leader in the global packaging industry. Successful implementation of aggressive expansion strategies has allowed Amcor to further leverage its global influence.

Leading research in recyclable material strengthens Amcor’s position against stricter environmental law.

However, there are several potential weaknesses, including Amcor’s increased debt level and its high exposure to raw material price fluctuation.

Nevertheless, with high profitability and an upward trend in the packaging market, Amcor is a good stock with high growth potential at a justified price.